As I have elucidated previously, 2022 was not a great year, and I am preparing for a 2023 recession. My reasoning is simple: interest rates are high, inflation remains high, and unemployment has bottomed and will likely head higher. Add in the inverted yield curve, and declaring a recession is a certainty for 2023.

How does one invest in a recession?

You could short various stocks. That’s a risky business because the most you can make shorting is 100%, and volatility can wipe out your gains in a bear market rally.

Tesla is down 75% since April 2022; that was a great short candidate, but will it fall another 75%? The time to make that trade was last year.

I do have a position in SH – ProShares Short S&P500 so if the markets crash quickly, I have a position. However, this ETF aims to seek a return of -1x the return of its underlying benchmark (target) for a single day, so this is not a long-term hold. If the market slowly grinds lower, even though you have guessed the direction correctly, the time premium and expenses will erode your gains.

So, shorting is a game best left to the experts. This brings us to the next area to consider during a recession:

Bonds

For the last ten years, interest rates have dropped to stimulate the economy. As inflation picked up, the Feds began raising interest rates starting in March 2022. Headline inflation remains high; unemployment remains low, so additional interest rate increases are likely between now and March 2023. Bonds are inversely proportional to interest rates, so as interest rates increase, bond values drop.

However: headline inflation and unemployment are lagging indicators. Employers hire and fire employees based on future expectations; there is a significant time lag. Employers don’t lay off employees at the first sign of trouble. It’s expensive to hire and train employees, and severance is expensive, so employers only begin layoffs when it’s obvious that they need to cut back.

I, therefore, expect to see one or two more interest rate increases. By March or April, it should be obvious that we are in a recession, so the Feds will stop raising interest rates, and during that pause period (not a pivot, just a pause), bonds will become the “go-to” investment.

I have taken a small position in TLT – iShares 20+ Year Treasury Bond ETF, and will add to it on further weakness. TLT pays a dividend, which is nice, but the big win will be later in the year when interest rates begin their inevitable decline.

So if shorting is too risky, and bonds are too early in the cycle to invest it, where should you park your money?

Cash

During periods of volatility and uncertainty, cash is king.

But wait, if inflation is high, cash is bad because your purchasing power is eroding. That’s true, but I believe inflation has already peaked, so inflation is less of a concern going forward.

So do you leave your cash in a bank account? No, bank accounts pay very low interest, so that’s not a great option. Here are some suggestions:

CASH – Horizons High-Interest Savings ETF. This low-risk ETF invests in high-interest deposit accounts with Canadian banks. It’s currently yielding around 4.75%, so as a risk-free asset, that’s good. What’s the problem? The problem is that if you bank at TD Bank, you can’t buy this ETF because it competes with TD Bank’s deposit products. (I suspect that CASH invests in TD Bank deposits, but they are doing it at a large scale, so they get a better interest rate than TD’s customers, which is why TD won’t sell it to their customers). I use TD as an example, but this is also true for other banks.

Also, although cash ETFs are investing in Canadian bank deposits, they are not CDIC insured, so there is some minimal risk.

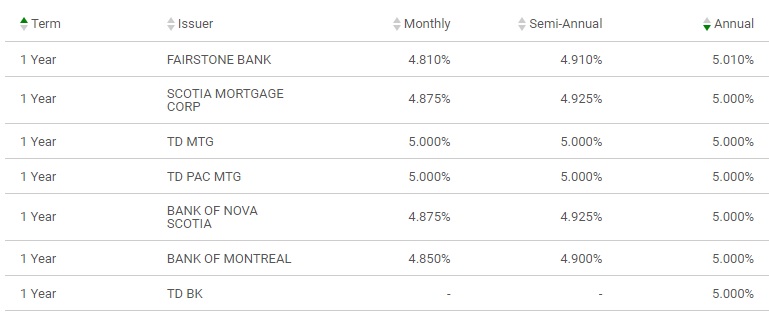

This leaves us with the simple alternative: GICs.

Every bank has them. The trick is to decide on your time horizon. With a one-year term you can easily get a 5% return, but there is some risk (from TD Bank’s website):

If you don’t want to lock in for a year, you can get 3.35% on a cashable one-year GIC. That may be the best option, particularly if rates are likely to increase in the next two months. You buy now, and then cash out and buy again in two months if rates are higher.

That’s my current thinking.

I also think gold will do well this year, but I’ve taken enough of your time for today, so perhaps we’ll discuss that next week.

Thanks for reading, and keep your seat belts fastened for a bumpy ride in 2023.

Cash is King, but What is Cash?

by JDH on January 7, 2023

As I have elucidated previously, 2022 was not a great year, and I am preparing for a 2023 recession. My reasoning is simple: interest rates are high, inflation remains high, and unemployment has bottomed and will likely head higher. Add in the inverted yield curve, and declaring a recession is a certainty for 2023.

How does one invest in a recession?

You could short various stocks. That’s a risky business because the most you can make shorting is 100%, and volatility can wipe out your gains in a bear market rally.

Tesla is down 75% since April 2022; that was a great short candidate, but will it fall another 75%? The time to make that trade was last year.

I do have a position in SH – ProShares Short S&P500 so if the markets crash quickly, I have a position. However, this ETF aims to seek a return of -1x the return of its underlying benchmark (target) for a single day, so this is not a long-term hold. If the market slowly grinds lower, even though you have guessed the direction correctly, the time premium and expenses will erode your gains.

So, shorting is a game best left to the experts. This brings us to the next area to consider during a recession:

Bonds

For the last ten years, interest rates have dropped to stimulate the economy. As inflation picked up, the Feds began raising interest rates starting in March 2022. Headline inflation remains high; unemployment remains low, so additional interest rate increases are likely between now and March 2023. Bonds are inversely proportional to interest rates, so as interest rates increase, bond values drop.

However: headline inflation and unemployment are lagging indicators. Employers hire and fire employees based on future expectations; there is a significant time lag. Employers don’t lay off employees at the first sign of trouble. It’s expensive to hire and train employees, and severance is expensive, so employers only begin layoffs when it’s obvious that they need to cut back.

I, therefore, expect to see one or two more interest rate increases. By March or April, it should be obvious that we are in a recession, so the Feds will stop raising interest rates, and during that pause period (not a pivot, just a pause), bonds will become the “go-to” investment.

I have taken a small position in TLT – iShares 20+ Year Treasury Bond ETF, and will add to it on further weakness. TLT pays a dividend, which is nice, but the big win will be later in the year when interest rates begin their inevitable decline.

So if shorting is too risky, and bonds are too early in the cycle to invest it, where should you park your money?

Cash

During periods of volatility and uncertainty, cash is king.

But wait, if inflation is high, cash is bad because your purchasing power is eroding. That’s true, but I believe inflation has already peaked, so inflation is less of a concern going forward.

So do you leave your cash in a bank account? No, bank accounts pay very low interest, so that’s not a great option. Here are some suggestions:

CASH – Horizons High-Interest Savings ETF. This low-risk ETF invests in high-interest deposit accounts with Canadian banks. It’s currently yielding around 4.75%, so as a risk-free asset, that’s good. What’s the problem? The problem is that if you bank at TD Bank, you can’t buy this ETF because it competes with TD Bank’s deposit products. (I suspect that CASH invests in TD Bank deposits, but they are doing it at a large scale, so they get a better interest rate than TD’s customers, which is why TD won’t sell it to their customers). I use TD as an example, but this is also true for other banks.

Also, although cash ETFs are investing in Canadian bank deposits, they are not CDIC insured, so there is some minimal risk.

This leaves us with the simple alternative: GICs.

Every bank has them. The trick is to decide on your time horizon. With a one-year term you can easily get a 5% return, but there is some risk (from TD Bank’s website):

If you don’t want to lock in for a year, you can get 3.35% on a cashable one-year GIC. That may be the best option, particularly if rates are likely to increase in the next two months. You buy now, and then cash out and buy again in two months if rates are higher.

That’s my current thinking.

I also think gold will do well this year, but I’ve taken enough of your time for today, so perhaps we’ll discuss that next week.

Thanks for reading, and keep your seat belts fastened for a bumpy ride in 2023.